Despite escalating geopolitical tensions, particularly in the Middle East, the global economic outlook for 2026 remains broadly resilient. According to projections by the International Monetary Fund, the vast majority of the world’s economies are expected to record positive growth this year, with only a small number—fewer than ten—likely to experience contraction. This underscores a surprising degree of stability in the face of ongoing uncertainty, as countries adapt to shifting trade dynamics, energy disruptions and financial volatility.

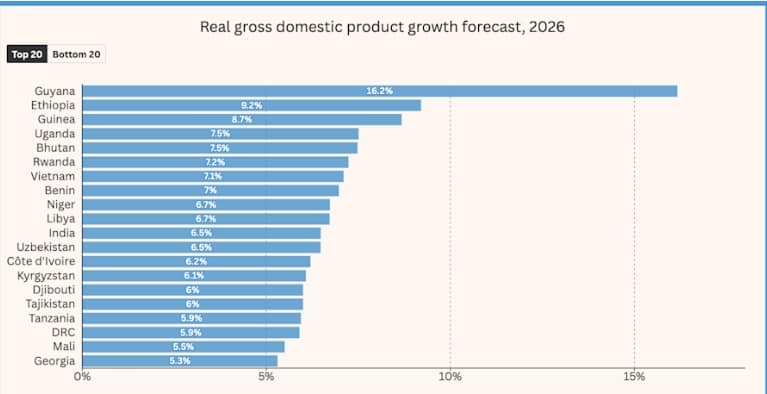

Among the standout performers are several emerging markets, which continue to outpace advanced economies in terms of growth. India is once again projected to lead the pack, driven by strong domestic consumption, a rapidly expanding digital economy and sustained government investment in infrastructure. Close behind is China, where policymakers are balancing structural challenges with targeted stimulus measures aimed at maintaining steady expansion.

Elsewhere, parts of Southeast Asia are also demonstrating robust momentum. Economies such as Vietnam and Indonesia are benefiting from diversified manufacturing bases, growing export markets and increased foreign direct investment. These nations have positioned themselves as key alternatives in global supply chains, attracting multinational companies seeking resilience amid geopolitical fragmentation.

In contrast, growth across many advanced economies is expected to remain modest. The United Kingdom and several European nations are grappling with lingering inflationary pressures, elevated borrowing costs and the indirect economic fallout of the Middle East conflict. Higher energy prices, driven by instability in a region critical to global oil and gas supply, continue to weigh on household spending and business investment.

The United States is forecast to maintain steady, if unspectacular, growth, supported by a resilient labour market and consumer demand. However, tighter monetary policy and global uncertainties are expected to temper expansion. Similarly, parts of the eurozone face structural constraints that limit their growth potential in the near term.

A key theme in the IMF’s outlook is the uneven nature of global recovery. While many economies are expanding, the pace and quality of growth vary significantly. Countries with strong domestic demand, diversified exports and stable policy environments are better positioned to weather external shocks. Conversely, those heavily reliant on energy imports or exposed to volatile financial conditions remain more vulnerable.

Ultimately, the 2026 growth landscape reflects both resilience and fragility. Even as conflict and uncertainty persist, most economies are finding ways to adapt and grow. Yet the path ahead remains complex, with risks ranging from geopolitical escalation to financial market instability continuing to shape the global economic trajectory.